AUDITOR’S OVERVIEW

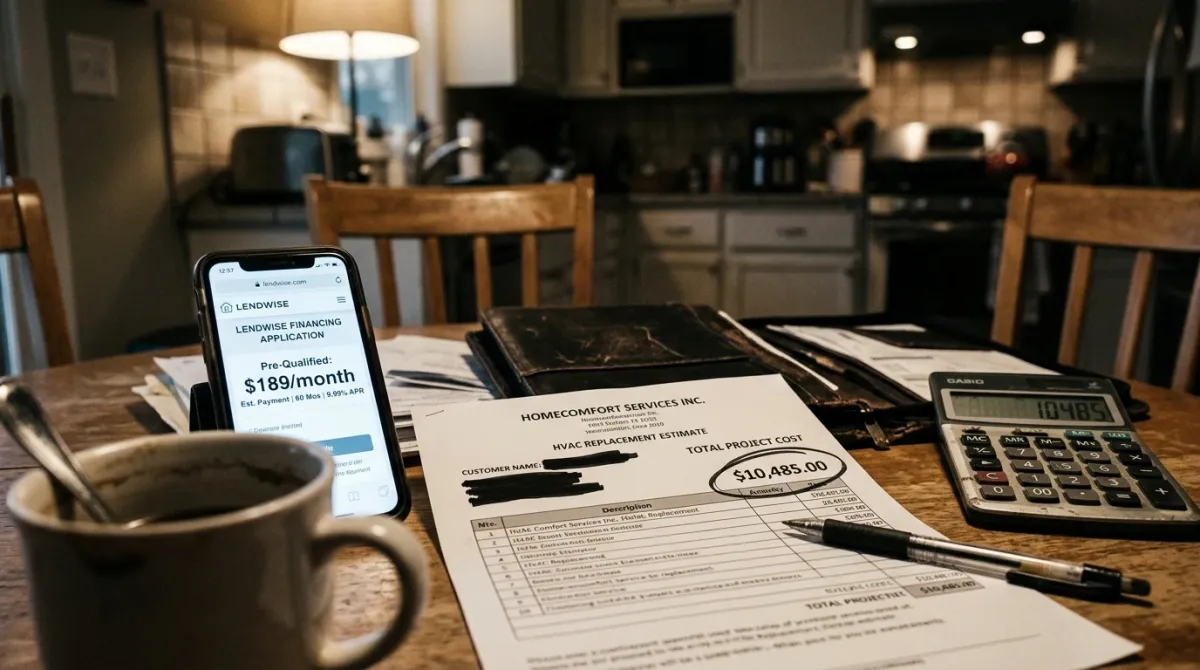

Financing changes whether a homeowner says yes to a $10,000 replacement quote. That part is uncontroversial — every operator who has watched a closed estimate convert because the customer found out monthly payments were $189 instead of one $10,000 hit understands the leverage.

What gets glossed over is the cost. The dealer fee on a 0% promotional loan does not come out of your margin. It comes off the top — straight off net revenue. A 9% dealer fee on a $10,000 ticket means the lender funds you $9,100 and you pay the cost of the homeowner’s “0%” promotion. If your gross margin on that job was $3,000, you just gave away 30% of your gross to enable the close. That can still be a win if the alternative was no sale at all. It is not a win if the alternative was a cash sale you could have closed without the financing.

This piece breaks down the three lender categories most HVAC operators encounter — Synchrony, GoodLeap, Wisetack — by structure, by credit tier, and by dealer-fee economics. The argument throughout: there is rarely a single right lender. The right answer is usually a mix sized to your customer base.

THE BOTTOM LINE

The three vendors named in this article each represent a different category of financing:

- Synchrony — revolving credit (a branded HVAC card), prime credit tier, low dealer fees on standard terms, higher fees on long 0% promos.

- GoodLeap — installment loan, originally focused on solar and now broad home improvement, prime-to-mid-prime tier, mid dealer fees.

- Wisetack — BNPL-style installment, mid-prime tier, structured for fast approval and shorter terms, mid dealer fees.

The structural difference is who they approve and what they cost the shop. The economic difference shows up in dealer fees, which can range from near-zero on full-APR loans to 12%+ on long 0% promos. Most healthy HVAC operations carry two or three lenders covering different credit tiers and pick which to present based on the homeowner’s situation, not based on which lender they signed up with first.

The Three Lender Categories

Revolving Credit — Synchrony

Synchrony Financial is the largest issuer of home improvement and HVAC private-label cards in the United States, with the Home & Auto segment disclosing tens of billions of dollars in receivables in its annual 10-K filings. The product is a branded credit card — “Carrier Comfort Card,” “Trane Home Improvement Card,” and similar — issued under a manufacturer or contractor partnership.

How it works: Homeowner applies through a quick credit check. Approved customers receive a revolving line of credit. Standard promotional structure: deferred-interest financing for 12-72 months. If the balance is paid off within the promo window, no interest. If not, retroactive interest from day one at a high APR (typically 25-30%).

Credit tier: Prime to mid-prime. Approval rates are reasonable for FICO 680+, more selective below.

Dealer fee structure (typical category ranges):

- 0% promo for 12-18 months: 4-7% of ticket

- 0% promo for 24-36 months: 7-9% of ticket

- 0% promo for 48-72 months: 9-12%+ of ticket

- Reduced APR (sub-promo): 2-5% of ticket

- Full APR / standard terms: 0-2% of ticket

Best fit: Prime-credit homeowners who will pay the balance within the promo window. Fast approval, fast funding, low operational friction for the shop.

Installment — GoodLeap

GoodLeap (founded 2003 as LoanPal, rebranded 2021) is a fintech lender originally focused on residential solar and expanded into broader home improvement, including HVAC. The product is a closed-end installment loan — fixed monthly payment, fixed term (typically 5, 10, 15, 20, or 25 years), fixed APR.

How it works: Homeowner applies through GoodLeap’s portal or via the contractor. Approved customers receive a single loan disbursed to the contractor. Monthly payments are fixed. No deferred-interest gotcha — the APR is what it is, throughout the loan.

Credit tier: Prime to mid-prime, similar to Synchrony but with installment risk-pricing.

Dealer fee structure (typical category ranges for installment lenders):

- Fair-value APR (rate close to market prime + spread): 0-3% of ticket

- Reduced APR (subsidized rate): 3-7% of ticket

- 0% promo / sub-prime promo: 7-15% of ticket

Best fit: Larger ticket sizes ($15K+ replacements, full-system installs with ductwork) where a long-term predictable payment is more attractive than a revolving promo. Homeowners who do not want a credit card opened. Solar plus HVAC bundled jobs.

BNPL Installment — Wisetack

Wisetack (founded 2018, partnered with Affirm for capital) is a Buy-Now-Pay-Later lender purpose-built for in-home services. The product is a short-to-mid-term installment loan, structured for fast approval and seamless homeowner experience at the kitchen table.

How it works: Homeowner receives a text link from the contractor at the time of estimate. Pre-qualification happens in seconds with no hard pull. If approved, the homeowner picks a term (typically 3-60 months) and the contractor is funded.

Credit tier: Mid-prime, more flexible than traditional bank lenders. Approval rates are higher in the 620-720 FICO range than Synchrony or GoodLeap typically deliver.

Dealer fee structure (typical category ranges for BNPL home services):

- Standard APR offers (homeowner pays interest): 0-3% of ticket

- Reduced APR offers (shop subsidizes): 3-7% of ticket

- 0% promo offers (shop subsidizes fully): 7-12% of ticket

Best fit: Mid-prime homeowners. Repairs and mid-ticket replacements ($3K-$15K). Operators who want a fast, low-friction kitchen-table close without a full credit card application process.

The Other Lenders Worth Knowing

The three above are the most-asked-about vendors in HVAC. The fuller landscape includes several others most operators end up evaluating:

- Service Finance Co. (now part of Truist). Installment loans for home improvement. Strong dealer network, broad credit acceptance, fee structures similar to GoodLeap.

- EnerBank USA (acquired by Regions Bank 2021, now Regions Home Improvement Financing). Long-established home improvement installment lender. Solid prime-tier acceptance.

- FTL Finance and Foundation Finance. Subprime / non-prime specialists. Higher dealer fees (often 12-15%+) but expand approval into FICO ranges below 600 where prime lenders decline.

- Manufacturer-branded financing programs. Carrier, Trane, Lennox, Daikin, Mitsubishi all have dealer programs that route through one of the above lenders under a co-brand.

The product set is bigger than the three names. The category logic — prime revolving, prime installment, mid-prime BNPL, subprime expansion — is the lens that matters.

The Dealer Fee Math (Modeled)

The number nobody wants to write on a marketing page: dealer fee comes off net revenue, not off margin. Here is the modeled math on a $10,000 AC replacement at 35% gross margin.

These are illustrative dealer-fee ranges, not exact published rates. Use them as a structural model, not as a rate sheet.

| Scenario | Dealer Fee | Net Revenue | Net Margin | Margin Hit |

|---|---|---|---|---|

| Cash sale | 0% | $10,000 | $3,500 | $0 |

| Standard APR loan | 1.5% | $9,850 | $3,350 | -$150 |

| Reduced APR loan | 5% | $9,500 | $3,000 | -$500 |

| 0% promo, 24-month | 7% | $9,300 | $2,800 | -$700 |

| 0% promo, 60-month | 10% | $9,000 | $2,500 | -$1,000 |

| Subprime expansion | 13% | $8,700 | $2,200 | -$1,300 |

The two real questions:

- Would the customer have closed without financing? If yes, every dollar of dealer fee is pure margin giveaway. If no, the dealer fee is the cost of acquiring the sale you would not have made.

- Is the dealer fee smaller than the gross margin gain from making the sale? A 10% dealer fee on a $10K job costs $1,000. If the alternative was no sale, the shop net is $2,500 of gross margin instead of $0. Easy decision. If the alternative was a cash close at the same price, the shop net dropped from $3,500 to $2,500 — a 28% gross margin hit.

The judgment moment for the technician at the kitchen table is reading which scenario is which. Most replacement closes that benefit from financing are scenario 1. Most repair closes under $1,500 do not need financing at all and pass dealer fees onto the shop unnecessarily.

Financing Is a Close-Rate Lever, Not a Margin-Free One.

Audit your estimate-to-close conversion and see whether financing is actually moving close rate or just shaving margin off cash sales.

AUDIT ESTIMATE CLOSE RATE →When Financing Helps and When It Hurts

Financing helps close when:

- The ticket is large enough that a homeowner cannot write a check ($5K+, often $8K+).

- The homeowner has stated cash-flow constraints during the conversation.

- The system is failing and the homeowner is shopping multiple quotes — financing eliminates the price-to-cash-on-hand mismatch.

- The customer is mid-prime credit and has been approved for a competing lender’s offer at another shop.

Financing hurts margin when:

- The ticket is small (under $1,500) — dealer fee per dollar of ticket is too high to absorb.

- The customer would have paid cash without prompting — financing is a structural giveaway with no incremental sale.

- The shop trains technicians to lead with financing rather than offering it situationally — leads to default presentation of subsidized offers on every customer.

- The shop carries only long-promo 0% offers (highest dealer fee tier) and never presents standard APR or fair-value options.

The behavioral pattern most operators miss: technicians on commission have an incentive to push financing on every close because financing increases the number of closes. The shop pays the dealer fee for every push. A close that would have happened in cash anyway, financed at 0% on a 60-month promo, costs the shop ~10% of the ticket in dealer fee for nothing.

This is one reason commission-pay-plan shops sometimes end up with higher financing attach rates and lower realized margin than salary-or-hourly shops at the same revenue level.

Why One Lender Is Almost Never Right

A single-lender shop trades simplicity for coverage. That tradeoff goes one of two ways:

Single prime lender (Synchrony only): Easy to operate. Decline rate is high in mid-prime and below. The customer who FICOs at 660 and gets declined by Synchrony walks away from the close — and probably walks to the competitor across town who runs Wisetack.

Single mid-prime lender (Wisetack only): Approves more customers, but on prime customers, the offers may not be as competitive as Synchrony’s 0% promo. The prime customer who could have closed at 0% / 60-month with Synchrony sees a 9.99% APR offer through Wisetack and hesitates.

The lender mix that holds up:

- Prime tier: Synchrony or Service Finance. Default offer for FICO 720+.

- Mid-prime tier: Wisetack or GoodLeap. Default offer for FICO 640-720.

- Subprime tier (optional): FTL or Foundation Finance. Reserved for FICO under 640 where prime lenders decline.

Run the prime offer first. If declined, soft-cascade to mid-prime. If declined again, present subprime if it makes sense for the ticket. Most operators who add a second or third lender see meaningful close-rate lift in the credit tiers their primary lender was declining.

How to Decide What’s Right for Your Shop

Six diagnostic questions:

- What percentage of your declined quotes had financing presented?

- What percentage of those presented financing offers got declined by the lender?

- What was the FICO range of the declined-by-lender pool?

- What percentage of your closed financing deals were 0% / 60-month or longer?

- What percentage of closed cash deals had financing offered first?

- Do you know what dealer fee category each of your closed financing deals fell into?

If you cannot answer questions 2-6, you are running financing without the data to evaluate it. The first move is not to add a lender — it is to track these numbers for 60 days.

The answers will usually point to one of three patterns:

- High decline-by-lender rate. Add a mid-prime or subprime lender to your stack.

- High share of long 0% promos. Reduce dealer fee burden by adding a fair-value offer to the standard presentation.

- High share of cash deals where financing was offered first. Train technicians to read the customer before defaulting to a financing pitch.

Most HVAC operations have at least one of those three patterns running unaddressed.

Frequently Asked Questions

What is a typical HVAC financing dealer fee?

Dealer fees vary by lender, credit tier, and promotional structure. Standard APR loans (where the homeowner pays interest at market rates) typically carry dealer fees of 0-3% of ticket. Reduced APR offers run 3-7%. 0% promotional financing — where the shop subsidizes the cost of the promo — typically runs 7-12% of ticket on prime lenders, and 12%+ on subprime lenders. The longer the 0% promo term, the higher the dealer fee.

Is GoodLeap or Synchrony better for HVAC contractors?

They serve different functions. Synchrony is revolving credit, fastest at point-of-sale, prime-credit-tier, and competitive on dealer fees for shorter promos. GoodLeap is fixed-installment, better fit for larger or longer-term tickets, and competitive on subsidized-APR offers. Most healthy HVAC shops carry both — Synchrony as the prime-tier card option, GoodLeap (or a comparable installment lender) for installment-loan customers and larger replacement tickets.

What credit score is needed for HVAC financing?

It depends on the lender. Synchrony and GoodLeap target prime credit (typically FICO 680+), with high approval rates above 720 and tighter underwriting in the 660-680 range. Wisetack approves further into mid-prime (often down to 620-640). Subprime lenders like FTL Finance and Foundation Finance approve into the 550-620 range with higher dealer fees.

How much does 0% HVAC financing cost the contractor?

Typically 7-12% of the ticket on prime lenders for 24-72 month promos, depending on term length. On a $10,000 ticket, that means the contractor receives $8,800-$9,300 from the lender after the dealer fee, with the homeowner paying $0 in interest if they pay off the balance within the promo window. The dealer fee is the cost of subsidizing the homeowner’s promo.

Should I offer financing on every HVAC quote?

No. Financing is a close-rate lever for tickets where cash-on-hand is the barrier — typically $5K+ replacements. Offering financing on small repair tickets (under $1,500) usually adds dealer-fee cost without incremental close. Defaulting to a financing pitch on every customer also gives away margin on cash closes that would have happened anyway. Train technicians to read the situation, not to lead with financing.

How do I increase my HVAC financing attach rate?

Three structural changes that consistently move attach rate: (1) carry a multi-lender stack covering prime, mid-prime, and optionally subprime credit tiers, (2) train technicians to present financing as part of every replacement quote above $5K, and (3) integrate the financing application into the kitchen-table sales process so approval happens before the homeowner has time to hesitate. The behavioral training matters more than the lender choice.

Is Wisetack a good fit for HVAC contractors?

Wisetack works well as a mid-prime installment offer alongside a prime card option. Its approval rate in the 640-720 FICO band is generally higher than traditional bank lenders, the kitchen-table application flow is fast (text link, no hard pull on pre-qualification), and the homeowner experience is mobile-first. As a sole financing option, Wisetack leaves prime-credit dollars on the table because its standard offers are less competitive than Synchrony’s 0% promotional financing on the prime tier.

Sources

- Synchrony Financial. Annual Report (Form 10-K). Discloses Home & Auto segment receivables and partnership program structure. synchrony.com/investors

- GoodLeap LLC. Public company information and product disclosures. goodleap.com

- Wisetack, Inc. Public merchant program information; partnered with Affirm for lending capital. wisetack.com

- Truist Financial Corporation. Service Finance Co. acquisition disclosures. truist.com

- Regions Financial Corporation. EnerBank USA acquisition and integration disclosures (now Regions Home Improvement Financing). regions.com

- Built on Tenth internal benchmark research on HVAC operator financing programs and dealer-fee structures, 2025-2026.

Methodology note: vendor-specific dealer fee rates are not consistently disclosed publicly and vary by promotional structure, volume tier, and credit acceptance. Dealer fee ranges in this piece are illustrative category ranges based on industry-typical structures, not exact rates from any single lender. Verify current dealer fee schedules directly with each lender before making program decisions. Attach-rate benchmarks across the HVAC industry are not publicly available with disclosed methodology — discussion of attach rate in this piece is structural and behavioral, not statistical.

Built on Tenth is an independent HVAC market intelligence firm providing objective, data-backed diagnostic reporting for HVAC operators. We do not sell advertising, accept referral fees, or offer marketing agency retainers. Our loyalty is strictly to the data.